Embedded B2B Payments

Convenient, fast, and secure payment options so your customers have everything they need to pay their invoices.

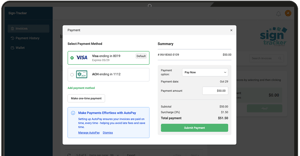

Get paid an average of 36% faster with the only AR automation and digital invoicing platform built for B2B companies. Features like automated workflows, customer collaboration, AutoPay, auto reconciliation, and enhanced data analytics reduce manual work and ensure on-time payments—every time.